Proverbs 19:1

(NLT): “Better to be poor and honest than to be dishonest and a fool.”

(ERV): “It is better to be poor and honest than to be a liar and a fool.”

(LBLA): “Mejor es el pobre que anda en su integridadque el de labios perversos y necio.”

(ESV): “Better is a poor person who walks in his integrity than one who is crooked in speech and is a fool.”

Sources:

(1) Achievable Study Resources

(2) Investopedia Article – Bearer Bond: Definition, How It Works, and Why They’re Valuable

(3) Congress.Gov – H.R. 4961 – Tax Equity and Fiscal Responsibility Act of 1982

(4) Transfer Agent – Investor.gov

(5) Zero Coupon Bonds– Investor.gov

(6) Money Market Securities – Investopedia Article

(7)

(8)

Bonds: The Basics

Bonds are loans. Bond issuers utilize bonds to raise money for construction projects, business expansion, and government expenditure.

Bonds are also a kind of debt security. Debt securities differ from both equity securities (common-stock & preferred-stock) & derivative securities.

The bondholder/investor becomes a creditor to the bond issuer.

Bonds are a type of fixed-income investment that provide a consistent annual/semi-annual stream of income to various bondholders.

Like most loans, bonds contain: (1) a principal amount borrowed and (2) interest. The principal is the original loan amount. The interest is the fee charged for borrowing the principal.

Unlike equitable securities like common-stock & preferred-stock, the Board of Directors do not need to approve a bond interest payment. If an interest payment needs to be issued, the issuer is legally required to pay the interest payment on the scheduled date. Non-payment puts the issuer at risk of arbitration & litigation.

The principal is the bond’s face value. The face value (principal) is the bond’s par value. These words: principal, face value, & par value are interchangeable when discussing bonds.

Most bonds begin in the primary market. Most bonds that begin in the primary market are issued at their par value.

Recall that a bond’s principal, face value, & par value are interchangeable.

Date of Maturity & Money Market Securities

All debt securities, including bonds, have a specific date of maturity. Some bonds have short dates of maturities that amount to a few days. Whereas, other bonds have longer dates of maturities that can last for over thirty years.

Bonds that have a date of maturity of one year or less can be known as money market securities.

When the date of maturity arrives, the bond issuer will make a final payment that often includes: (1) the principal/face/par value and (2) a final interest payment.

The Risks Associated With Bonds

Bonds, as with other debt securities, share unique risks. Some of these risks are systematic & others are non-systematic.

Typically, the longer the date of maturity the greater the risk of default/non-repayment. The more time an investor must hold on to a bond, the more risk & uncertainty can accumulate; whereas, bond-issuers with short-term maturities are less likely to default, all else being equal.

In most cases, short-term bonds have less risk than long-term bonds.

To compensate for the additional risk factor involved in a lengthier date of maturity, many issuers will offer a higher interest rate payment relative to the prevailing market interest rate.

Systematic Risks

As with most securities & investment vehicles, bonds are exposed to systematic risks. Systematic risks apply to the entire investment market. Systematic risks cannot be eliminated through investment portfolio diversification.

Some systematic risks that bonds are exposed to include: interest rate risks, inflation risks, and reinvestment risks.

Non-Systematic Risks

Not all risks are systematic. Non-systematic risks do not impact the entire investment market. Some non-systematic risks can be eliminated through investment portfolio diversification.

Some non-systematic risks that bonds are exposed to include: default risks, liquidity/marketability risks, legislative risks, and political risks.

Proverbs 19:20

(GNT): “If you listen to advice and are willing to learn, one day you will be wise.”

(AMP): “Listen to counsel, receive instruction, and accept correction, That you may be wise in the time to come.”

(LBLA): “Escucha el consejo y acepta la corrección, para que seas sabio el resto de tus días.”

(HCSB): “Listen to counsel and receive instruction so that you may be wise later in life.”

How Interest Rates are Set When Bond’s Are Issued In The Primary Market

The bond’s interest rate payments are based on the bond’s par value.

Interest rates are also known as the coupon or stated rate.

For example:

If a $1,000 par, 3.4% bond trades on the secondary market at $850, the interest rate payments will be based on the par value of $1000, instead of the market value of $850.

Question #1: Using the above example for values, what will the annual interest payment be in U.S. dollars?

Annual means yearly.

The annual interest payment is based off the bond’s par value.

Therefore, since the par value is $1,000 & the interest rate is 3.4%, the bond’s annual interest payment will be 34 dollars.

Question #2: Using the above example for values, what will the semi-annual interest payments be in U.S. dollars?

Semi-annual means the annual payment is split into two. Therefore, the annual payment of $34 will be divided into two payments of $17 each.

The secondary market value of $850 will not impact the interest rate payments.

Interest rate payments are based on the bond’s principal amount.

Recall the word principal is interchangeable with par value & face value.

Question #3: What are the Semi-annual interest payments (in U.S. dollars) on a $1,000 par, 7.8% bond trading on the secondary market at $1,110?

Interest payments for bonds are based on the bond’s par value.

This bond’s interest rate is set at 7.8% of $1,000. Therefore, this bond’s annual interest payment will be $78.

However, recall that semi-annual interest rates divide the annual interest rate payment into two separate payments throughout the year.

Therefore, this bond’s semi-annual interest payment will be $39.

Zero Coupon Bonds: While outside the scope of this article, some bonds have a 0% interest rate. These 0% interest rate bonds are known as Zero Coupon bonds.

Bonds: Digital Ownership

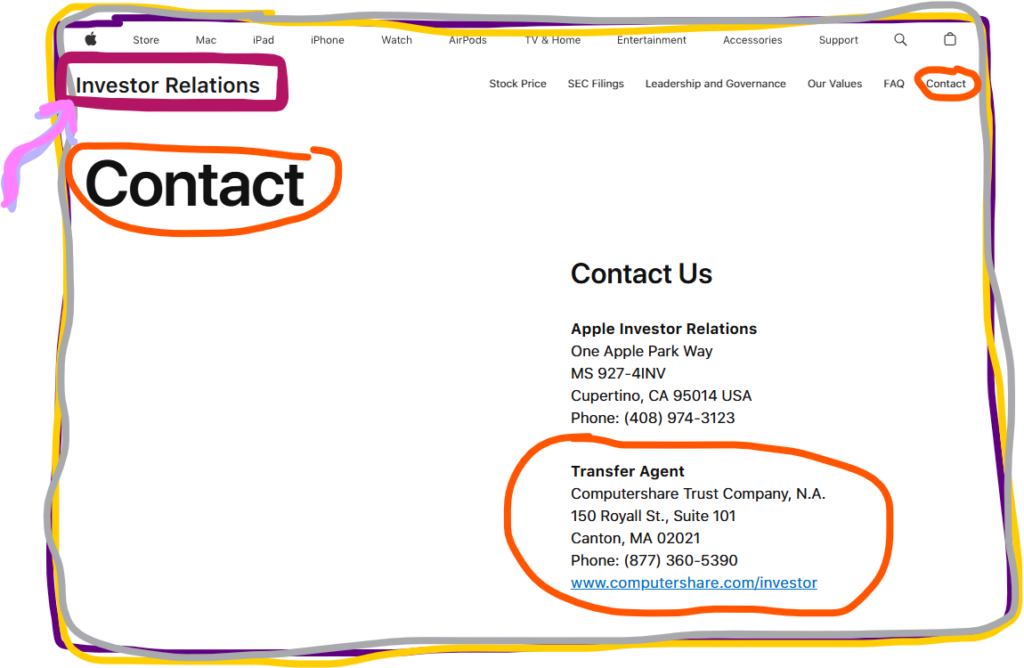

In the modern era, bonds are issued in a digital book-entry form.

There is often no physical certificate & ownership is recorded by a transfer agent in a digital database. Digital registration helps ensure that bondholders receive any interest payments due.

Many transfer agents are banks or trust companies. However, an issuing company can act as it’s own transfer agent. Many transfer agencies are required to register with either the SEC or a bank regulatory agency.

An issuing companies transfer agent is often found under the “Investor Relations” part of their website.

Here is an example from Apple’s Investor Relations website:

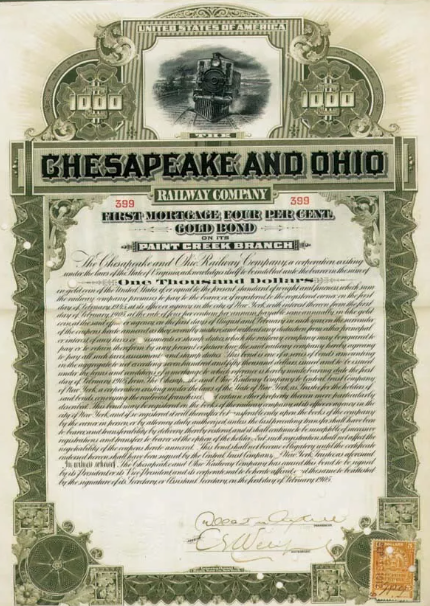

Bearer Bonds

Previously, bonds were issued in a physical bearer form. Whoever held the physical certificate had ownership of the bond. This concept is similar to physical cash. Some countries still issue physical bearer bonds, but the United States stopped issuing bearer bonds in 1982 through the Tax Equity & Fiscal Responsibility Act of 1982.

Some individuals utilized bearer bonds for “money laundering, tax evasion, and any number of under-handed transactions.” However, pre-existing bearer bonds can still be redeemed through the Treasury.

Types of Bonds

There are many different kinds of bonds:

US Government bonds, corporate bonds, municipal bonds, zero coupon bonds, secured bonds, full faith & credit bonds, and mortgage bonds.

Each of these bond types has different characteristics, strengths & weaknesses.

Proverbs 19:5

(ESV): “A false witness will not go unpunished, and he who breathes out lies will not escape.”

(LBLA): “El testigo falso no quedará sin castigo, y el que cuenta mentiras no escapará.”

(NLT): “A false witness will not go unpunished, nor will a liar escape.”

(GNT): “If you tell lies in court, you will be punished–there will be no escape.”

Leave a Reply